Aurora Cannabis Inc. (TSX:ACB)(NYSE:ACB) will be conducting a reverse stock split, effective May 11th, 2020, and CLN is here to let you know what that means, and what to expect.

The price will go up, and there will be fewer shares

When Aurora’s shareholders check their accounts on the morning of May 11th, they’ll have a single share for each group of 12 they held on May 10th, and the market will reflect the consolidation by pricing the rolled back shares at about 12x the ACB price May 10th.

“Reverse split” or “share consolidation” are the terms companies use to avoid having to call it a “rollback”, which tends to upset retail shareholders, who have memories of all the other rollbacks they’ve endured, none of which are any good.

Share consolidations are familiar events in the resource sector, where companies are formed to do mineral exploration that, even if successful, will produce no regular income at all. Investors buy shares in exploration stage mineral companies as a bet that a successful mineral discovery and development will be taken out by a larger company at a premium. The ones who aren’t taken out (and that’s most of them) have to keep financing until, eventually, there are so many shares with such little value that new money isn’t interested in anything but a majority stake.

The cannabis sector is newer but has already seen one epic consolidation that makes for a pretty good example.

Remember Pasha Brands?

CLN readers may remember our January 2020 coverage of Pasha Brands (CSE:CRFT), which had spent the prior seven months doing all-stock deals with every home-grown cannabis brand who didn’t know any better, ballooning its share count to 194 million shares from zero in what might be record time. Pasha was halted at $0.08 when we published that. It undertook its own 12:1 rollback March 27th, resumed trading March 31st, opening at $0.40, and closing at $0.11 that day. It now trades very low volume around $0.07, right around where it started pre-consolidation. President and Chairman Patrick Brauckman resigned on April 7th.

With 16 million shares outstanding post rollback at $0.07, the next raise that Pasha conducts will surely make the current shareholders – including the people in the BC cannabis community who vended their companies to Pasha for shares, insignificant. Another 16 million shares issued at $0.07 would raise about $1.1 million (less fees). Pasha burned through $12.7 million in cash through September 30th of 2019 alone. Raising that much again would print 181 million Pasha shares, diluting of the pre-rollback Pasha shareholders put together down to a collective 8% stake.

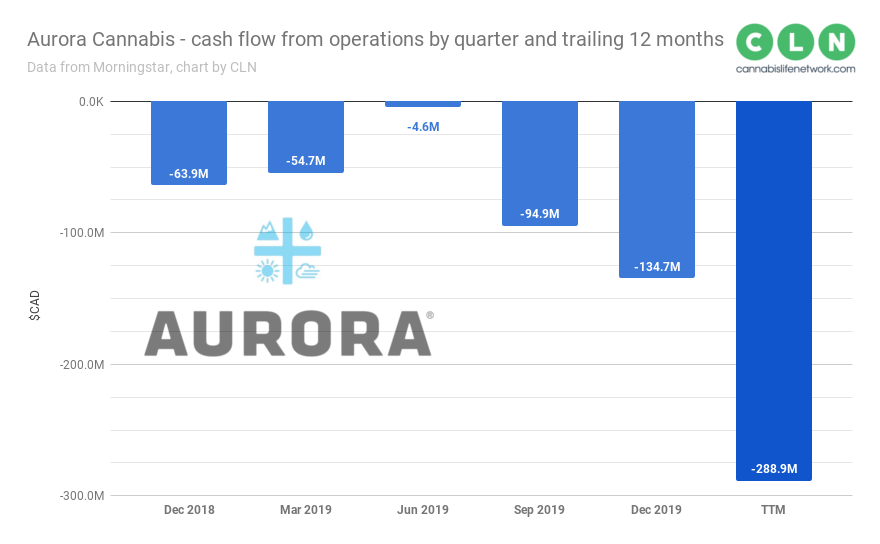

Bleeding Cash

Following the consolidation, Aurora will go from having had 1.3 billion shares outstanding to having 100 million shares outstanding, and the reason they’re doing it is the same reason they had 1.3 billion shares outstanding in the first place.

Aurora isn’t a zero-cash penny-dreadful like Pasha Brands: it’s a multi-license producer capable of volume. But Aurora is an animal of the cannabis equities bubble. Its operations have never been cashflow positive on their own, don’t figure to become cashflow positive any time soon, and won’t be worth anything at all if they cease to operate, so Aurora is going to need some cash to float the turnaround effort.

It also has to service and repay ~$600 million worth of debt. Between the optics of having to do a 300 million share raise to get the cash they need in the near term and an NYSE requirement that the stock remain above $1 to keep its listing, the Aurora journey needs to make a detour through rollback city before it fuels up.

Could a rolled-back Aurora be a buy after it’s been financed?

CLN doesn’t give investment advice, but we’re happy to point out that the financial media apparatus that helped to over-value ACB in the first place hasn’t shut down yet. This very bullish article from investorplace.com’s David Mondel kicks off with a bold lie in the nut graph, telling its readers that Aurora has “…a trailing 12-month price-to-earnings ratio of 4.06,” while, in point of fact, Aurora has negative earnings, and therefore no P:E at all.

Mondel goes on to make a weak case that Canadians might order more cannabis while they’re on quarantine, as if any serious cannabis consumers were ever buying product from Aurora in the first place. The article was published April 16th, two days after the 12:1 consolidation was announced, but makes no mention of it.

Aurora closed at $0.93/share on 14 million shares of volume on the TSX Thursday, April 16th. It is scheduled to be rolled back 12:1 May 12th.